The Largest Government Pension Fund is Investing Overseas: Is it an Ironic Move for the Japanese?

January 17, 2015

Akira Kondo

|

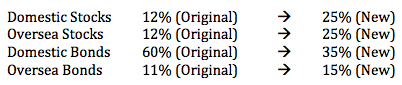

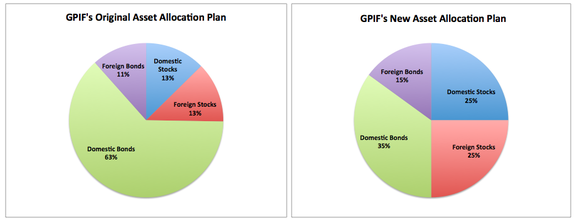

In November 2014, Japan’s Government Pension Investment Fund (GPIF), the largest pension fund in the universe, rolled out its plan to expand asset purchases overseas. With $1.1 trillion assets under GPIF’s management, its planned exposure into oversea markets may become favorable over the U.S. equity markets. The GPIF’s asset allocation before the announcement and its future new asset allocation are as follows:

Source: Government Pension Investment Fund of Japan

According to the GPIF’s new asset allocation plan, its significance mainly comes from a huge cut back of the domestic bonds, which today accounts for 50 percent or about $550 billion value (as of the end of September 2014). The GPIF plans to decrease its share of domestic bonds into the 35 percent target from the original 60 percent or from today’s 50 percent. It would generate additional $163 billion worth of cash from the future sale of the domestic bonds to fund the other asset classes, such as domestic stocks, oversea stocks, and oversea bonds. Specifically, $75 billion goes to domestic stocks, $84 billion goes to oversea stocks, and $32 billion goes to oversea bonds out of the $163 billion cash generated after the sale of domestic bonds (assuming no short-term assets).

|

|

|

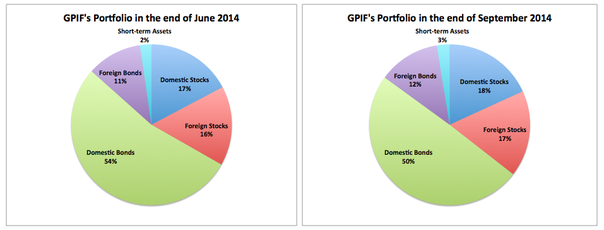

Over the past months, the GPIF’s asset allocation has been in progress but by the stock markets’ strength. Its domestic bonds holding declined to 50 percent in the end of September 2014 from 54 percent in the end of June. In the meantime, a share of domestic stocks rose to 18.2 percent from 17 percent, a share of oversea stocks climbed to 17.4 percent from 16 percent, and a share of oversea bonds increased to 12.1 percent from 11 percent.

|

Source: Government Pension Investment Fund of Japan

|

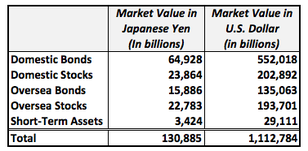

Exchange rate: 117.62JPY/USD as of Jan. 17, 2015

|

|

The move made by the GPIF is intriguing among economists as well as investors because a highly risk-averse Japanese pension fund is now going to take higher risks by accumulating the riskier asset classes, such as stocks, in its portfolio after trimming the safer domestic bonds into almost half. Although the GPIF’s move yields higher risks, it is also riskier to hold onto the well less than 1 percent yield of the Japanese government bonds (less than any 30 year maturity bonds) while the central bank of Japan is targeting a 2 percent inflation rate over coming years. Plus, owning Japanese currency may be becoming troublesome as the currency weakens daily basis while in the massive quantitative easing in progress by the central bank of Japan.

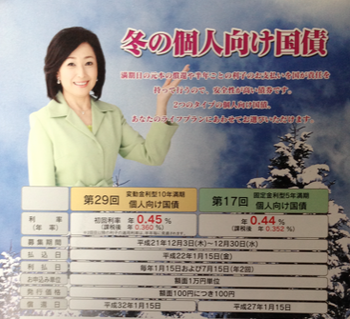

A typical Japanese government bond prospect at one of many banks in Japan. A 10 year and a five year Japanese government bonds offer 0.45 percent and 0.44 percent yields, respectively. There is only 1 basis point (0.01%) difference between them, which one would you choose, five years or 10 years? In fact, they are the most popular financial products to own for the Japanese. A typical Japanese government bond prospect at one of many banks in Japan. A 10 year and a five year Japanese government bonds offer 0.45 percent and 0.44 percent yields, respectively. There is only 1 basis point (0.01%) difference between them, which one would you choose, five years or 10 years? In fact, they are the most popular financial products to own for the Japanese.

Over $80 billion out of the $162 billion cash position from the sale of domestic bonds into the oversea equities over coming years, the U.S. stock market should gain some momentum through the GPIF’s new asset allocation. Although the GPIF does not specify what country’s stocks it has purchased or it is going to purchase, globally popular U.S. equities are probably the top pick for the GPIF thanks to a gradual recovery of the U.S. economy. As it is a pension fund, it is not wise for them to purchase individual stocks, such as Apple and Boeing. Rather, it will purchase ETFs that cover a large-cap market, such as SPDR S&P 500. For Japanese equities, the GPIF would target an ETF, such as Black Rock’s iShare Nikkei225. Therefore, most components of the S&P 500 should be benefited through the GPIF’s massive purchases over next years.

Is that $80 billion really a lot? It is hard to say because the biggest market-cap company, like Apple, can return more than $100 billion worth of capital to its investors by offering stock buybacks and dividends. However, with that $80 billion cash, it can buy a whole company of eBay, Costco, or Starbucks, whose market-caps are $63 billion, $61 billion, and $60 billion, respectively. Again, the GPIF may not purchase individual stocks but buy ETFs, which contain solid companies that can return capitals to shareholders. While the GPIF’s move to shift its asset allocation from the domestic bonds to oversea assets seems favorable to the U.S. investors, it is, on the other hand, quite an ironic situation for the conventional Japanese investors. They own Japanese debts, long-term Japanese bonds through banks, over past many decades but the government-oriented GPIF is now shifting its allocation to oversea stocks and bonds after the continuing sales of Japanese government debts. If it were the situation, where the Bank of Japan led the GPIF to sell the Japanese bonds and own oversea assets, the Japanese investors, who have been owning the debts till now, would be simply left behind. On the flip side, it has been taken as a message that the GPIF or the Japanese government asked the Japanese to invest in stocks both domestically and globally to increase their wealth by themselves, like what Americans do in their 401k accounts.

Again, the GPIF’s move to increase its exposure to stocks domestically and internationally generates higher risks. If the value of the portfolio were hit hard due to plunging stock prices worldwide, who would compensate the loss of the fund? However, the GPIF has to take higher risks to operate the fund while ageing population in Japan is now in full swing. Plus, it requires higher returns through its new asset allocation to keep up with the possible higher inflation rate in the future. The second largest fund in the universe is Norway’s Norges Bank, which operates $700 billion under its management, and its exposure to stocks, including both domestic and international, is 60 percent while bonds and real estate account for 35 percent and 5 percent, respectively. Norges Bank invests across the countries to diversify its equity holdings. The GPIF should do so and it could increase its oversea stock allocation even higher while cutting back the domestic stocks. Investing in the largest economy, like the United States, is probably the safest place to own stocks, rather than investing in an uncertain future Japanese economy. As long as its uncertainty and the Bank of Japan’s massive money injection into the markets continue, the value of the Japanese currency continues to plummet against major hard currencies. It is wise to own oversea stocks and bonds to take advantage of owning more foreign currencies or to mitigate the risk of owning its own currency. Japanese economy is still far from the recovery mode while experiencing the economic contraction past quarters after the sales tax hike in last April. However, the stock market is still trying to move higher thanks to the weakening Japanese Yen.

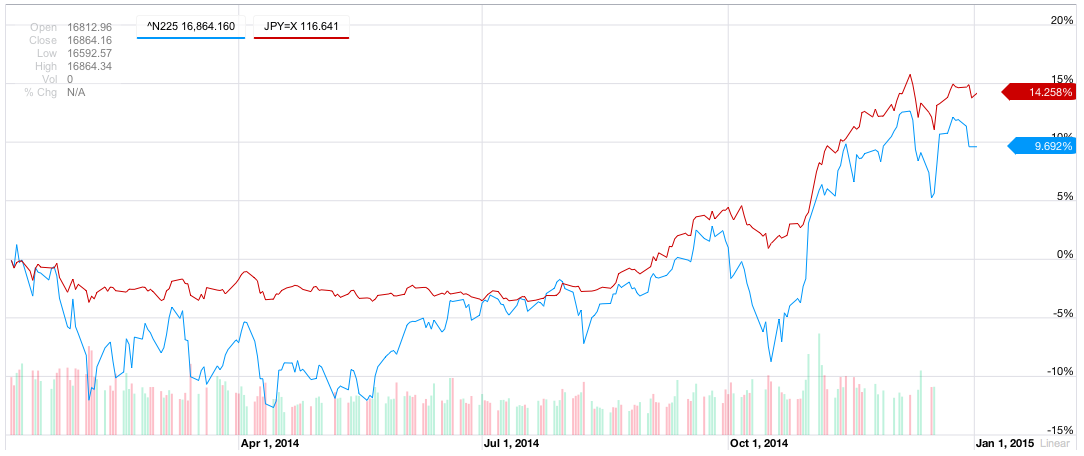

Japan's Nikkei 225 Index climbed nearly 10 percent in 2014 while Japanese currency depreciated 14 percent. Source: Yahoo! Finance

|

More GPIF story is available in Japanese <Click here to read>

|

|

This bull market condition will not continue unless the Japanese economy is firing all cylinders to generate higher output. Without higher production, the wages remain the same while the consumer prices across the market increase and eventually the Japanese stock market itself starts to struggle after generating 34 percent gain since the Bank of Japan Governor, Kuroda, took the office in earlier 2013 or generating 65 percent gain since the Prime Minister, Abe, was re-elected in the end of 2012. Whether it is late for the GPIF to jump onto the market momentum now or not, it is still considered to be a wise move, especially its new allocation to oversea stocks and bonds, which later consist of 40 percent of the GPIF’s asset. The generation-to-generation pension fund probably has the highest patience among any investors and that patience the GPIF has may yield the reward in the long run.

Sources: Government Pension Investment Fund of Japan, http://www.gpif.go.jp/en/. Norges Bank, http://www.nbim.no/en/investments/. |